I think the most interesting part of market analysis is human behavior because so much of what happens in the markets can be explained by human emotions. One of the more fun elements (fun is relative here considering I am talking about investing) is the “Magazine Cover Indicator created by Legg Mason strategist Paul McRae Montgomery. What he found was when it came to the markets, magazine covers turned out to be a contrarian indicator. The logic behind it goes like this: By the time a particular investment trend reaches the cover page of a major publication, it is so widely embraced by the public that “everyone is in” – i.e., there is no one left to perpetuate the trend. Therefore, the trend is close to reversing… often with a vengeance.

Based upon a story reported by Freemarketcafe.com (now nondollarreport.com), Bloomberg Businessweek holds title to the most infamous cover story ever. In August of 1979, the cover of Businessweek proclaimed “The Death of Equities.” As it turned out, equities were far from dead. In fact, they were on the verge of a major rebirth. Stocks bottomed early in 1980, before taking off on the biggest bull market in history. Just three years after this cover story appeared, the S&P 500 index had doubled. And three years after that, the S&P 500 had tripled.

But in the dark days of the late 1970s building up to the infamous Businessweek cover, the stock market had gone nowhere for more than a decade, most investors believed that stocks were a dud.

“The masses long ago switched from stocks to investments having higher yields and more protection from inflation,” the Businessweek article observed. “Now the pension funds – the market’s last hope – have won permission to quit stocks and bonds for real estate, futures, gold, and even diamonds. The death of equities looks like an almost permanent condition – reversible someday, but not soon.”

Twenty-three years after the “Death of Equities” cover story, Businessweek cemented its “indicator” credentials for all time by running a cover story titled “The Angry Market.” During the two years that preceded this story, the stock market had been very angry indeed. An epic bear market had erased nearly half the S&P 500′s value. But during the two years that followed this story, the S&P soared more than 40%. Three years later, it was up 60%, and five years later, it was up 100%. In fact, the S&P hit the exact low of its 2000-2002 bear market on the day “The Angry Market” cover story hit the newsstands!

Businessweek does not corner the market in being a timing expert. In September 1977, Time Magazine’s cover story warned, “Sky-High Housing.” And while it’s true that American home prices had doubled over the preceding decade, home prices would double again over the following decade… and would quintuple by 2005!

Then, in June of 2005, just as this once-in-a-lifetime housing boom was ending, Time hit the newsstands with a cover story titled “Home Sweet Home: Why we’re going gaga over real estate.”

“Ah, the blistering real estate market,” its story gushed, “where dreams of big bucks come wrapped in aluminum siding… Your house is now your piggy bank, ATM and 401(k)… Folks brag about having bought their home in the ’90s the way they used to brag about having bought Microsoft in the ’80s. Even if you’re not contemplating buying or selling anytime soon, the amazing lift in home values is changing the way we think about the roofs over our heads. Real estate isn’t so much about nesting today as it is about nest feathering.”

But at that very moment, the spectacular American housing boom was already on its way toward an equally spectacular bust. Condominium prices topped out in the identical month this Time cover story appeared – June 2005. Single-family home prices topped out shortly thereafter.

“Homebuilding stocks went a bit higher during the month or so subsequent to that cover story,” Paul MacRae Montgomery relates. “[But] from that point, they crashed 78%-90%… Housing prices [fell] a more modest 28%… But this drop was still enough to constitute the worst drop ever in home prices – worse than in the Great Depression.”

Not content to be dead wrong twice about the housing market, Time went back to the well one more time. On the cover of its September 6, 2010, issue, the magazine declared, “Rethinking Homeownership: Why owning a home may no longer make economic sense.”

“Homeownership has let us down,” the cover story lamented. “For generations, Americans believed that owning a home was an axiomatic good… A house with a front lawn and a picket fence wasn’t just a nice place to live or a risk-free investment; it was a way to transform a nation… [But] The dark side of homeownership is now all too apparent: foreclosures and walkaways, neighborhoods plagued by abandoned properties and plummeting home values… If there ever were a time to start weaning America off the idea that homeownership cures all our ills, now… would be it.”

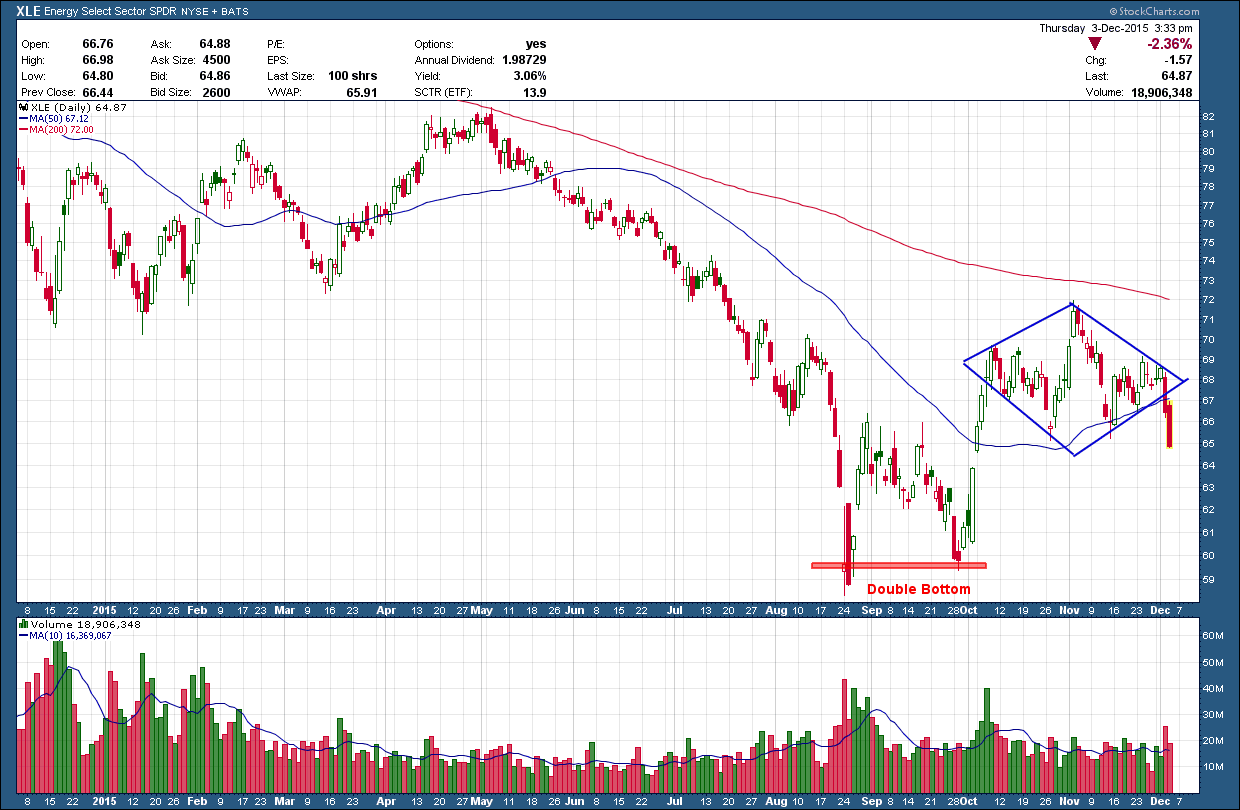

There are dozens of examples, the above are but just a few. With that as a background I would like to show the August 31, 2015 cover from Bloomberg Businessweek regarding the headline story “The China Bears”.